The Walmart Credit Card stands out for shoppers hoping to maximize savings and enjoy smoother checkouts at both physical stores and online.

This guide breaks down what makes Walmart credit cards unique, details the application process, and shares practical insights for anyone considering this financial tool.

Walmart Credit Card Basics

Understanding the basics helps set reasonable expectations.

Main Types of Walmart Credit Cards

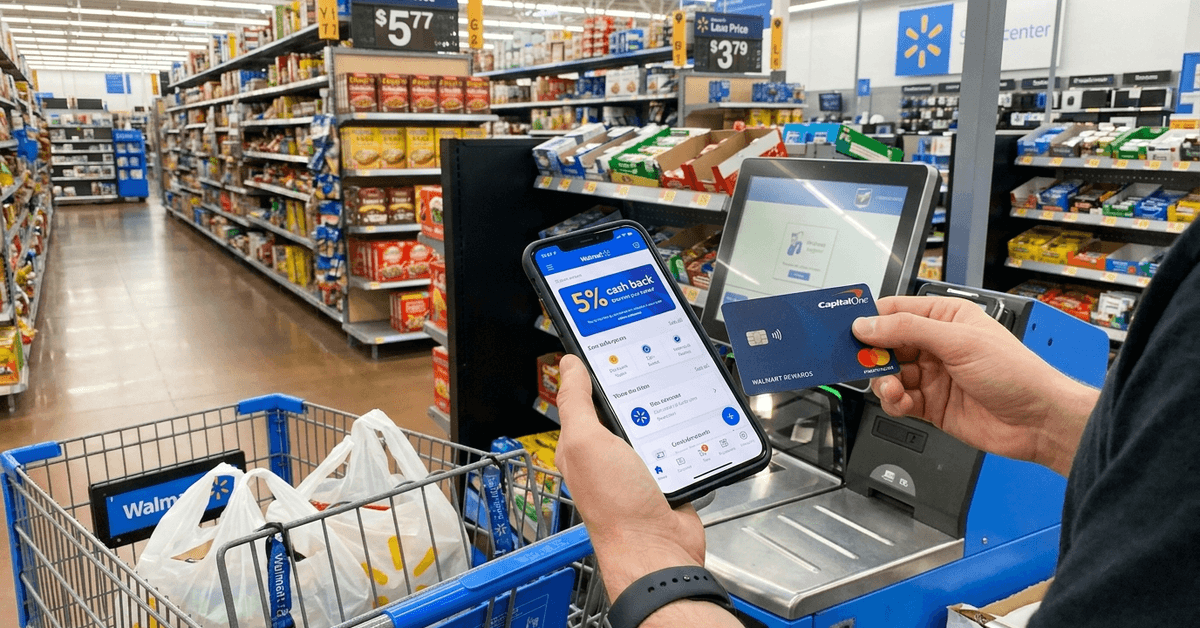

- Walmart Rewards Card: Used only at Walmart stores and websites.

- Capital One Walmart Rewards Mastercard: Accepted anywhere Mastercard is accepted.

Both cards offer rewards for purchases, but the acceptance and redemption flexibility differs.

Rewards and Benefits Overview

- Earn points for purchases made at Walmart.com, in-store, and through their mobile app.

- Special rewards rates often apply to grocery pickup and delivery via Walmart’s site.

- Some categories outside Walmart also earn rewards with the Mastercard version.

Payouts usually arrive as statement credits, gift cards, or travel redemptions. Redemption rates can sometimes shift. Checking terms frequently helps avoid surprises.

Basic Eligibility Requirements

- Stable income, typically verifiable by pay stubs or bank statements.

- A fair or better credit score (typically 640+ for the Mastercard version).

- Valid U.S. address and Social Security Number.

- Applicants must be 18 or older.

Customer service representatives can clarify gray areas if unsure about qualification.

How the Walmart Credit Card Application Works

Applying has never been easier, with several options for convenience.

Where to Apply

- In-store at checkout or customer service desks.

- Online via the official Walmart credit card website (usually links through Capital One’s secure portal).

- Using the Walmart app if you already have an account.

Online applications tend to be the fastest. Physical applications may appeal more to those wanting face-to-face clarification.

Step-by-Step Application Process

- Gather financial and identification documents, such as photo ID and proof of income.

- Navigate to the application interface (online or in-store terminal).

- Enter all requested details, including name, address, Social Security Number, and income.

- Review your information before final submission to minimize delays.

- Submit and wait for an instant decision or follow-up communication, which may take a few days if further verification is needed.

Most approvals or declines are instantly provided online. If not, status updates typically arrive by email or mail within a week.

What Happens After Approval

After approval, you can expect account setup details, card delivery information, credit limits, payment instructions, and guidance on using available benefits.

- Receive your new card by mail. Setup instructions arrive with it.

- You can often use the card for Walmart purchases while waiting for the physical card if approval is in-store.

- Setting up online account access immediately is recommended to track spending and manage rewards.

Understanding Walmart Credit Card Rewards

The rewards program has clear perks, though there are some restrictions.

Points Structure

- 5% cash back on Walmart.com purchases, including grocery pickup and delivery.

- 2% cash back for in-store Walmart purchases, Murphy USA, and Walmart fuel stations.

- 1% on all other Mastercard-eligible locations (for the Mastercard version).

Some promotional rates may apply for new users, such as an introductory 5% cash back in-store for the first 12 months when using Walmart Pay.

Reward Redemption Options

- Redeem points for Walmart gift cards, travel, statement credits, or to cover a purchase directly at checkout.

- Minimum redemption thresholds may exist, so checking the rewards dashboard helps.

Walmart’s app offers easy tracking, which is convenient for regular earners wanting full usage out of their points.

Managing Your Walmart Credit Card Responsibly

Responsible use maximizes value and avoids unnecessary costs.

Best Practices for Cardholders

- Monitor statements monthly to ensure correct charges and posted rewards.

- Pay off balances in full to avoid interest charges, as rates can be higher than expected.

- Set alerts through the Capital One app for payment due dates and suspicious activity.

- Utilize additional features like free credit score tracking and fraud protection.

If a mistake is noticed, contacting customer service promptly can often resolve issues before they worsen.

Common Pitfalls to Avoid

- Carrying high month-to-month balances can result in accumulating significant interest charges.

- Missing even a single payment can negatively affect your credit score.

- Failing to read reward expiration rules might mean losing out on earned perks.

Some users suggest creating a spreadsheet to track purchases and payments. This habit adds another level of organization.

Comparing Walmart Credit Card to Other Options

Walmart’s cards are competitive, but alternatives might fit different spending habits or locations.

Comparison Table: Walmart vs. Other Store Cards

Comparing Walmart’s store card with other retail cards can help you evaluate rewards, fees, eligibility, and everyday shopping benefits.

| Card | Acceptance | Rewards | Annual Fee |

|---|---|---|---|

| Walmart Credit Card | Walmart only or worldwide (MC edition) | Up to 5% at Walmart | $0 |

| Target REDcard | Target stores | 5% at Target | $0 |

| Amazon Store Card | Amazon.com only | Up to 5% at Amazon | $0 |

| Chase Freedom Unlimited | Worldwide | 1.5% everywhere | $0 |

Each card has its strengths. Walmart’s is arguably best for frequent Walmart shoppers, especially those using grocery delivery.

Security and Account Protection Features

Keeping financial information safe is a top priority with Walmart and its issuing partners.

Key Security Features

- Zero fraud liability for unauthorized purchases.

- Instant card lock features through the Capital One mobile app.

- Consistent account monitoring for suspicious activity with prompt alerts.

Most fraud issues can be resolved with a phone call or app notification.

Tips to Enhance Your Own Security

- Change your card’s PIN regularly, especially after suspected data exposure.

- Never share card details via phone or email unless confirming the legitimacy of the request.

- Monitor for phishing attempts targeting Walmart or Capital One users.

Staying vigilant can prevent headaches tied to card misuse.

Application Troubleshooting and Support

If occasional issues arise during application or use, solutions are generally available.

Common Application Hurdles

- Errors in entering information.

- Disputes over address or income verification.

- Technical issues with the online portal.

Walmart and Capital One both provide several support channels, like live chat, dedicated phone lines, and mail support options for complex cases.

Useful Support Tools

- Capital One mobile app: Manages cards, rewards, payments, and security settings.

- Walmart app: Useful for tracking orders and managing purchases but not for credit management directly.

- Online customer service portals, both on Walmart.com and the Capital One website.

Users have found that live chat is often the quickest for minor account questions, while phone support works best for more complicated disputes.

Conclusion: Making an Informed Choice

Choosing the Walmart Credit Card can be a smart decision for many frequent shoppers, but it’s not for everyone.

The rewards structure stands out for Walmart.com and grocery pickup fans. However, those who shop broadly might prefer a card with wider flat-rate rewards.

Whatever the decision, understanding the rewards, potential pitfalls, and everyday management tools ensures a better experience. Careful comparison—alongside staying informed of updates to terms and features—sets users up for success.

Note: There are risks involved when applying for and using credit. Consult the bank’s terms and conditions page for more information.